Money Mountaineering is my new book where I explore the world of money and provide my views on its nature and the challenges we all face as we try to survive, even thrive, in this complex, uncertain, noisy and sometimes irrational wilderness.

So, is this another financial advice book? Not exactly, rather this is a book designed to help you understand what kind of advice you truly need. My goal is to help you gain a better understanding of the financial world you must live in and what you must do to make your way through it.

In particular, I want to help you determine:

What you can decide for yourself- almost certainly more than you’ve been led to believe.

Where you need help- probably in different areas than you think.

What trustworthy sources are out there- fewer than you might hope.

This book is not for those who are “too rich to care,” nor will you get much value from this book if you have no financial resources at all and worry about simply getting by from one day to the next. This book is for the vast numbers of people who are in the middle; those who struggle with the trade-offs between saving for retirement and saving for a down payment on a house. It is for those who can’t decide whether to pay off a student loan early or “double down” and borrow more to start a business. It is for those about to retire who need to figure out when to take Social Security, how much to withdraw from their 401(k) accounts, and whether to downsize their home or take out a reverse mortgage to supplement their retirement income. It is for anyone who has a complicated financial life in which it’s not only challenging to find answers but it also isn’t clear what questions to ask.

You won’t find any easy solutions to your financial problems in this book. You may find, however, that this book will give you the ability to ask the right questions, and as a result, begin to make better choices.

Think of the world of money as a dangerous and unknown mountain wilderness full of unseen perils, inhabited by wily predators of all sorts. You have found yourself stranded and lost, and in addition to simply surviving and figuring out where you are, you also want to make your situation as comfortable and stress-free as possible so you have the time, energy, and resources to make the best of the rest of your life.

Having been around the Insurance Industry for over 40 years, I have learned a few things about the business model that has kept large carriers alive and profitable for decades and sometimes centuries (several of the big ones have been around since the 19th century).

One of the key principles I have seen in operation is that hazards almost never turn out as bad as policyholders fear – except when they turn out much, much worse. As a result, insurance companies are able to charge premiums that will generate a profit but do need to attend to the possibility of a “black swan event” that could be truly catastrophic. Fundamentally much of insurance is based on the fact that even though we live in a “fat tailed” world where the mean is far greater than the median, most consumers, even the most sophisticated ones, operate as if risks follow a Normal distribution. In a sense this creates a win-win situation where policy holders feel they are getting risk protection at a reasonable price, while the carriers, with their huge cash reserves, underwriting protocols and re-insurance treaties to protect them from catastrophe, continue to make a good profit collecting premiums in excess of claims.

When it comes to this pandemic, we can see this principle at play in real time. COVID-19 is a quintessential black swan, and when it came ashore early last year, I along with many other actuaries, tried to figure out just how bad this scourge was and most importantly, how bad was it going to get. My particular focus was on COVID-19 mortality, in part because it seemed to be the one aspect of the pandemic that was more tractable than the others (i.e., people are either alive or dead) and partly because mortality risk is so central to the health of the Life Insurance Industry.

It was tricky because data was hard to come by and the disease itself was poorly understood. Nevertheless, in June of last year, I put together an analysis of COVID mortality and published an article on how many people would ultimately die of the disease. My conclusion was that by the time a vaccine was generally available 475,000 people would have died from COVID. The article is available here.

My conclusion, which I believe has proven correct, was that this disease is terrible, but not quite as terrible as people feared. Most pundits at the time were expecting deaths to be well over a million before the pandemic ended, and while my article was well received, there were many who thought I was being overly optimistic about the future course of the pandemic.

With the pandemic now easing its grip on us and vaccines beginning to be generally available, I thought it was time for a follow up analysis.

An updated analysis of COVID mortality

Late last summer, I had actually begun to look at how my projections were turning out and was somewhat disturbed to find that the CDC data I had relied on was becoming messy and difficult to parse. In particular, beginning with some County health departments in Texas, the definition of what constituted a “COVID-19 death” began to shift from “dying from COVID” to “dying with COVID” (i.e., even if you die from a stress induced heart attack after having contracted the disease you are included in the count). You can read about how and why the change was made here. I don’t doubt that this change was made with the best of intentions, but unfortunately when you change definitions like this, analysis becomes much more difficult.

The good news is that Life Insurance companies are primarily interested in the fact that a death occurred rather than the specific reason for the individual’s demise. As a result, when I took a fresh look at the data, I focused on the number of “extra deaths” that we have experienced as a result of living (and dying) with the disease. I also talked at length with my colleagues at various life insurance companies to find out how worried they were about any “underwriting apocalypse” that might befall the industry.

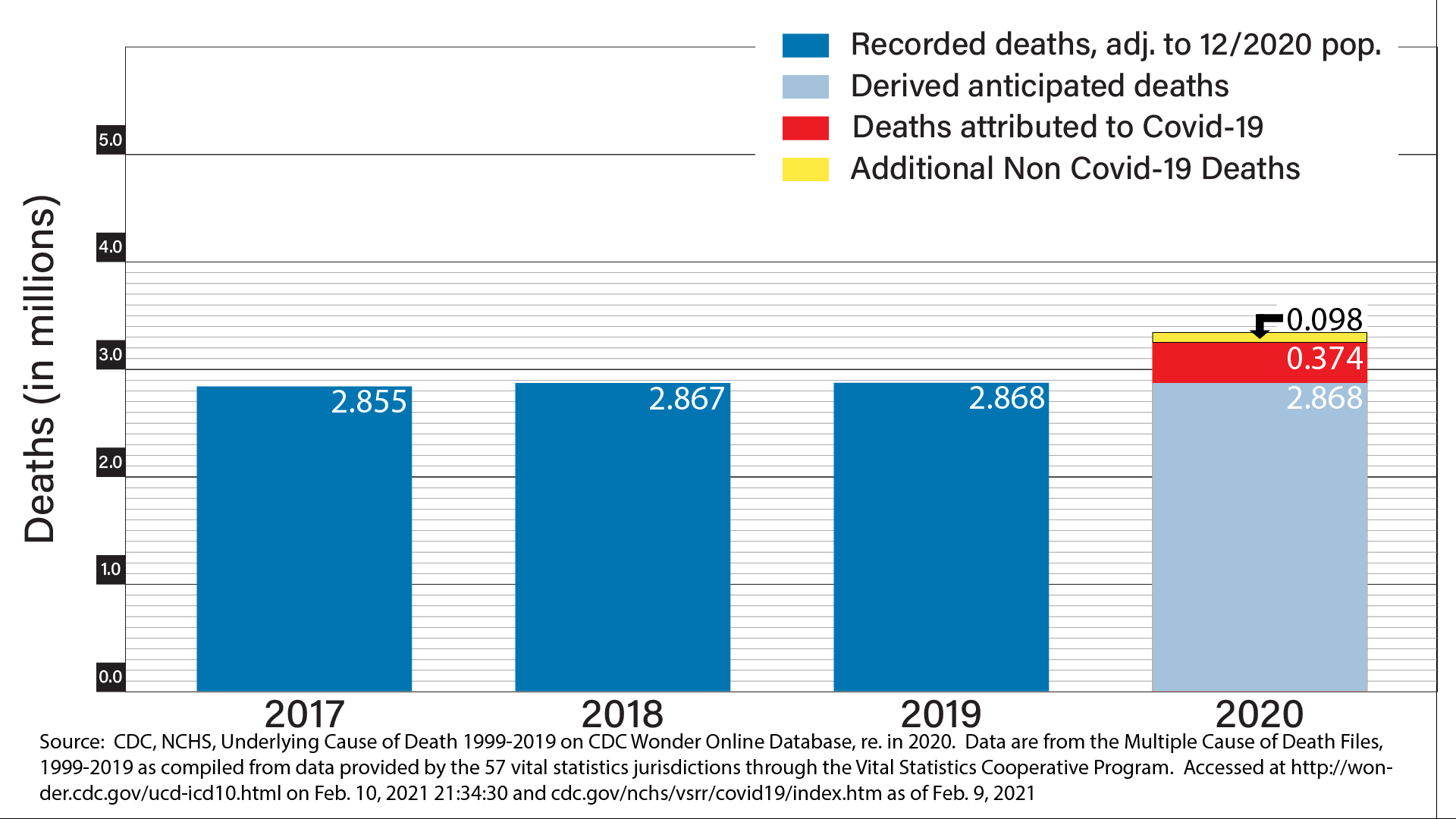

It turns out that the CDC continues to keep very good data on total deaths even though the number of “COVID deaths” for reasons noted above is pretty noisy, and in particular very difficult to use to compare the direct impact of the virus in the autumn to that experienced during the early part of the year. To address this challenge, I developed a baseline of “normal deaths” and compared that to what happened in 2020 which differed from prior years due to the presence of the virus in our midst. This effort was complicated because of various factors including population growth and the normal seasonality of mortality (November- March generally being the most lethal months), but in the end, I believe I was able to at least see the big picture of what is going on.

By comparing deaths in 2020 to those in 2017-2019 (adjusting for population changes in the last 4 years), I found that while the number of reported COVID deaths in 2020 was 374,121 (a mix of those dying “from” and those dying “with” the disease) there were 472,116 “excess deaths” relative to what we would actuarially expect during 2020. The difference between these two numbers (97,995) is the number of people who died from the indirect effects of the pandemic. In my June article, I had looked at this and found that in the early days of the pandemic, there were actually less total people dying of non-COVID causes than expected, mostly due to reduced auto accidents and flu deaths. While this was good news, I speculated then that once the effects of deferred medical care and economic hardship began to affect mortality, we could see this trend reverse. It seems that this has happened, and the important question now is whether these secondary effects will persist or fade away when the pandemic ends. The chart below summarizes these numbers and notes where the data comes from.

374,121 COVID deaths and 472,116 excess deaths are both big numbers, but when we really look at the impact of this increased mortality risk on the Life Insurance industry, we find that the current financial impact is very mild and no one within the industry whose career depends on it seems particularly worried. I am not sure why this is the case, but my guess is that because those that died because of the pandemic had less life insurance than the average American.

That is not to say, that Life Insurance companies are ignoring COVID, but at least within the product lines that I am most familiar with, i.e., Corporate Owned Life Insurance (COLI) and Whole Life Insurance, what I am seeing is modest adjustments in underwriting standards and virtually no changes in the premiums that policyholders are being asked to pay.

I recently spoke with some of the executives at major carriers to get their view of COVID’s impact on their life insurance products. What they told me was that as a general rule, underwriting issues around COVID mortality are far less a concern than the continued low interest rate environment and the potential for Corporate income tax rates to increase substantially under the new Democratic administration. It seems that both of these macroeconomic factors pose greater challenges and opportunities for the industry than the prospect of many more COVID deaths. That being said, the industry is responding to all three of those aspects of the current environment.

With respect to the two economic issues, the folks I talked to are quite optimistic about the future of COLI. With higher tax rates, COLI will become a much more tax efficient corporate financing vehicle for numerous purposes, and while chronically low interest rates make “fixed” products perform worse, insurance companies are responding by shifting resources toward their “variable” products where recent stock market performance has made those products particularly attractive.

With respect to COVID specifically, it appears that claims have not materially increased during the pandemic, perhaps due to the sad fact that many of those who have died from the disease had limited or no life insurance. In any event, from a carrier perspective, the COLI business has not suffered at all, though at least some carriers are taking certain steps to guard against potential “antiselection” and other factors that may impact profitability if COVID surges again. Specifically, carriers are deemphasizing their corporate sponsored products (i.e., life insurance that employees choose to obtain with subsidies from the company) and focusing more on its corporate owned products (COLI, corporate owned annuities, and life insurance for groups of executives).

As I noted at the beginning, actuaries have a terrific record in evaluating and managing mortality risks, and Life Insurance companies continue to be some of the most solid and stable companies in the Financial Services sector of the economy. The clarity with which the industry has viewed the risks posed by COVID thus far gives me hope that the industry will continue to thrive.

However, the number of people who have died as a result of the disruption of our economy and healthcare delivery system that COVID has caused as well as the possibility of a resurgence of the disease in future years does suggest that actuaries and underwriters need to continue their vigilance regarding this risk if Life Insurance is to continue to play the critical role it has in providing financial security and stability to both individuals and corporations in the future.

If history is any guide, they will, and Life Insurance will continue to provide the financial security and stability to consumers and corporations alike that it has for over a hundred years.

I walk a lot these days – not because I need to, but because it keeps me close to the land

You see, a month ago I lost my land along with my home and everything in it.

It was the eve of Yom Kippur and when I woke that morning there was the familiar smell of smoke in the air. Living in rural Sonoma County I’ve become accustomed to the environment we now live in – Threats to health and welfare lurking all around us — unseen but still palpable and very real.

I checked the source of the smoke and found that the fire was just outside of Calistoga town of 5000 about 20 miles due east of me. That was concerningly close, but the wind was blowing south and in between it and me lay the town itself as well as miles of forest and Hood Mountain , a 2700 ft peak at whose base my 8.5 acre homestead lay, nestled against a spring fed creek that runs all year and up which salmon still swim.

Throughout the day I kept track of what was going on near Calistoga. Soon the fire had been named, and while that meant it had become a major problem, the news was still relatively encouraging in that Cal Fire was making this one a priority and was deploying an enormous amount of resources to containing it and limiting its impact on the people who lived in Napa county where the fire was centered. I had been through this too many times before, including in 2017 when the Nuns Fire came within a mile of my property and so I was concerned but not overly so. I was confident that I and my neighbors would not have a problem with the fire itself though there was always the possibility that PG&E would shut off our power to prevent it from spreading. I was half-expecting that soon I would be getting a “prepare to evacuate” or even an “evacuation warning” text, but my phone is filled almost to capacity with those messages received over the last few weeks since fire season began, so while I don’t ignore them, I had, unfortunately, gotten too used to false alarms and was therefore wholly unprepared for what came next

Some time in the middle of the afternoon, things took an ominous turn. A light dusting of ash started raining down on us and the quality of the air began to deteriorate badly. It took some time for us to figure out that the wind had shifted and that the fire was getting closer. This is when I made my next mistake. I assumed that since Calistoga was between me and the fire that if there was any danger, I would get plenty of warning because all those residents would need to evacuate first and that would give me plenty of time to get ready. It never occurred to me that the fire might simply go around the town and head straight for Hood Mountain.

Feeling worried, but in need of some grounding I attended my temple’s online Kol Nidre service – in some ways the most important holy day of the Jewish year. The service ended at 7:30 and by then the evacuation warnings were creeping closer.

I went to find my contractor Patrick, a brilliant and resourceful ex-football player from Georgia who was staying on my property while working on adding a bathroom and an outdoor kitchen to one of the out-buildings on my property. Having only been in Sonoma since June (he had come to visit my caretaker and find some work in the area), this was his first California fire season and even though I warned him that a wildfire was nothing to mess with, he seemed supremely calm and in control. I told him that the fire seemed to be headed our way and as he surveyed the property he said that he thought that we would be ok, but he was going to start cleaning up the job site “just in case”.

Then things began to both speed up and to move in slow motion. A little after 8:30 an evacuation warning came through and I knew it was time to act. And here is where I made my final and most costly mistake. Instead of gathering stuff and packing, I spent the next precious 20 minutes walking through my house trying to decide what I would take if and when an actual evacuation order came. I asked Patrick if we had any boxes so I could start packing and he said that he thought there were some around, and while I started poking around, my mind fruitlessly started evaluating and prioritizing, mentally packing and trying to estimate what would fit into my pick up truck and what I would have to leave behind because it was too bulky.

Then suddenly I was out of time.

At 9pm the evacuation order came, and now there was no mistaking what was happening. The fire was climbing up the back side of Hood Mountain and if it came down the other side we were in real trouble — right in the fire’s path backed up against a thick forest so tangled and overgrown that even walking through it on a normal day is a struggle. I couldn’t imagine how Cal Fire could possibly stop it if it ever got that far.

I was freaked, but at least I was now moving and acting. I had frittered away all my margin, and now could only grab and go. I got my passport, birth certificate, my will and a few other documents laying loose on my desk. I grabbed as many pictures of my family I could throw into the one large suitcase I’d found and threw a few clothes into a gym bag that was lying on my bedroom floor. I made sure I got my laptops and some notebooks containing notes for my unfinished book manuscript, and on the way out I was able to pick up a couple of pieces of memorabilia like an album of my 1960’s baseball cards and a couple of Grateful Dead relics, but that was it.

I texted a friend in Berkeley to make sure I had a place to go and then asked Patrick help me load the truck. At 9:15 I was driving down our private dirt road and eventually onto Los Alamos, then across 12 onto Melita road taking the back way to 101 to avoid the rush. I got onto the highway just in time to get a frighteningly urgent follow up call from Sonoma County telling me to run for my life and as I headed south towards Berkeley I passed a huge line of fire trucks coming up from Marin to fight the fire.

Meanwhile, despite my pleas that he evacuate as well, Patrick stayed to try and save my house. Why he risked his life to save the home of someone he had only met a few weeks ago is still one of the great mysteries in my life, but stay he did. For hours he fought desperately to save my house, hosing down the deck, digging fire breaks and moving equipment and lumber out of the way of the flames that were now on the land burning my stables and the redwood deck next to it. He worked side by side with the Cal Firefighters until after midnight when even he had to surrender to the overwhelming awesome power of nature’s fury. At the last minute he threw some tools into his little Mazda and drove through the flames right behind Cal Fire who themselves had just abandoned my home to fall back and fight the fire from Los Alamos a mile down the road.

It was only days later that I got the full story from Patrick. It seems that the fire came roaring down the mountain and then vacuumed through the little valley around the creek exploding into a firestorm that consumed everything along our dirt road only slowing down when it hit the pavement where Wildwood Trail becomes a public road. Patrick never had a chance, and yet some combination of courage, heroism and bull-headed stubbornness kept him fighting a hopeless battle against impossible odds until it was truly a question of living or dying. I am profoundly grateful he chose life, as otherwise I could never forgive myself for letting him stay and try to save my home.

Now three weeks later, I finally have a little space to call my own – a tiny studio apartment near downtown owned by Marta, the kind woman who runs a vintage clothes store in Railroad Square. She and others like her are what makes this community what it is and why I call it home. There is Linda who is an old Deadhead like me and still sells antiques out of a barn near town and there is her boyfriend Leo who lost everything he had in the fire as well but somehow still smiles and offers help to anyone who needs it. They had me over for a hot meal in her backyard the other night and even though they have each suffered grievous losses this year, they opened their house and their hearts to me. There is something uniquely wonderful about this town and the people who live here. Probably it comes from the fact that most of these folks have deep roots in Sonoma County and the catastrophes that keep visiting this place simply bring us all closer and make us more committed to look out for each other.

Wherever it comes from, Santa Rosa is a very special place and gives me hope for the future.

I walk a lot these days, not just because it keeps me close to the land, but also because it keeps me close to the people of this town and of this county. Even though COVID has made it dangerous to get too close, we are finding our way – to joy, to gratitude, to curiosity and to connection. Maybe we are even moving toward something a little lighter than the stormy darkness that surrounds us. Only time will tell.

I wanted my property to be a sanctuary – I’d even opened up a bank account to make it so. Valley Oak Sanctuary is the name I gave it in honor of the dozens of centuries old Oaks that lived on my land. Happily, many of them survived. My vision was for the property to become an island of peace and safety amidst the anger, conflict and danger that seems to surround us. That vision will now have to be deferred – at least for a while

And yet I know that Valley Oak Sanctuary will emerge once again, and while I don’t know when, how, or in what form it will take, I do know where it will be – at the end of a dirt road by a creek at the base of Hood Mountain. Hopefully it will happen soon, and while I can’t yet focus on rebuilding, when it happens, you will know. I won’t keep it a secret.