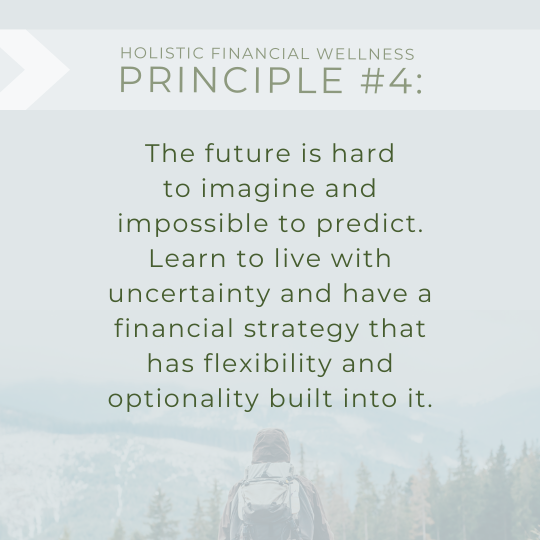

As I started to write about the 4th fundamental principle of Holistic Financial Wellness, I realized that while many of the 6 HFW principles I espouse are more and less applicable in our lives at different times, the need to be able to live comfortably with uncertainty as you make financial decisions that have significant consequences for your future while also entailing painful costs in the present may be, for many, many people, the most important principle of all right now.

I considered lots of stories and lots of different aspects of making decisions under uncertainty to illustrate what I wrote in Section III of Money Mountaineering, but in the end I decided to address the “elephant in the room” and talk about the two parts of our human nature that can hijack our judgment and ability to make good financial decisions when the stakes are significant and the outcomes are multiple and highly uncertain.

.

.

Hustling Chess, Overcoming Fear and Getting Curious

A few weeks ago, I went to New York City where I visited one of my favorite spots – the park at the south end of Union Square where the chess hustlers make their living charging nominal fees for lessons to those who appreciate their skills and winning money over the board from those who don’t. When I lived in Westchester and worked in NYC in the 1990’s I spent many hours getting to know these unusual characters and was able to learn a few traps and tactics that let me scare a few masters in the weekend tournaments I used to play in during my time in the City.

One of my favorite denizens of that world is a man named “Po” — a wise, funny and fast talking player of near International Master strength who never lets his customers know quite how strong he is. Po has beaten almost all of the current generation of young grandmasters, catching them as prodigies on the way up (e.g. Hikura Nakamura, Irina Krush and many others). To hear him tell it, his “lessons” helped a few future stars learn some practical tricks that fueled their rise to the top.

Like many great chess players, Po has a distinct world view and a well-articulated philosophy on how to survive on the chess board and in life. When I asked him what he thought of the current state of the world and what he suggested people do amidst all the confusion and chaos that seems to surround us, he paused and then gave me some wisdom that he passes on to both his friends and his customers. He said that the important thing was to not be afraid – not of your opponent or the all the unseen threats that might lurk on the board. He thought that most people are suffering now because “they opened their eyes and found that it is still too dark to see”.

For me, not only is that great advice, but it highlights perhaps the greatest challenge we face in living with “not knowing” and making good financial decisions despite all the uncertainty of the future and the incomplete information we have about the present.

Decisions over the chessboard are often not that different than the financial decisions I speak about in Money Mountaineering. Both entail making choices whose long term (and even short term) consequences are often impossible to predict and not even a grandmaster will be able to understand all of the aspects of a given position, let alone the plans and strategies hidden within the mind of the opponent sitting across the board. Curiosity and an ability to be openminded enough to consider many possible futures at one time is critical to becoming a good player.

For financial decisions this is even more important. Fear is the enemy of curiosity, and curiosity is what will allow you to identify the important things you can figure out and those that you can only make educated guesses about. It will help you identify the areas where a financial expert can explain aspects of your decision that you need to understand and will allow you to absorb the information that the expert provides. Overcoming fear and becoming curious will help you identify the aspects of your decision that can never be determined and allow you to make better choices.

As I learned from working with Annie Duke, whose expertise is poker not chess, the key is to make smart bets and then recognize that no bet on the future is a sure thing.

So, take it from Po. Even though you might be scared of the dark and can’t see what is down the road, that doesn’t mean you shouldn’t proceed forward, gathering the clues, getting help where you can and making the best financial decision you can with the information you have and the range of possible outcomes that the future presents.

Unfortunately, overcoming fear is not enough, and to truly be comfortable with “not knowing” you also need to overcome at least one other bit of psychological baggage that most of us carry, and for that I want to talk about what I learned from a different teacher.

Marilee Adams and the “Learner Mindset”

Marilee Adams is a writer friend who I got to know several years ago at a 3-day authors retreat sponsored by Berrett Kohler, the company that published my first book and several of Marilee’s. Marilee’s books have been hugely popular and despite our different statuses in the world of books and book sales, Marilee took an interest in my ideas and gave me a great deal of advice and support all throughout my process of writing Money Mountaineering.

In addition to having had the same publisher for our books, it seems that my suggested approach to the unknowability of the future is quite similar to aspects of Marilee’s advice on how to address uncertainty in general and how to gather enough information to make good decisions. As with many of my fellow authors, I had scanned Marilee’s book, but until this Spring I had never had the time to read it cover to cover.

That changed earlier this year when Marilee invited me to be a guest at one of her 4 week/8 session workshops on how to “Change Your Questions and Change your Life”. I didn’t have to think twice before accepting her generous offer because, in addition to the prospect of getting to watch how Marilee works her magic on large groups who flock to her usually sold-out workshops, I also sensed that her message to adopt a “Learner Mindset” when facing important life decisions might be very relevant to what is embodied in my 4th foundational principle of Holistic Financial Wellness. These two factors made it a very easy decision to devote the minimum 12-hour time investment to attending the workshop.

It turns out that adopting the Learner Mindset is not exactly the same as what I mean when I write about becoming comfortable with the uncertain future, but had I not gone to the workshop I would never have realized quite how important it is not to fall prey to anticipation, a state of mind that can lead you to make bad decisions – particularly financial ones.

Just like fear is the enemy of curiosity, I think anticipation is the enemy of open-mindedness. If you think you know what is going to happen (good or bad), then you can’t be open to the range of possible ways in which the future might unfold. And that is exactly what anticipation is — expecting something specific to happen while closing your mind to all the other possible paths the future might take.

This was not news to me, but during the workshop, Marilee went pretty deeply into what generates anticipation in us and what we should do to not let it bite us. And even though I have thought about uncertainty and how to deal with it for decades, I learned something important from Marilee and am grateful to her for reframing the problem of our tendency to think we know what will happen instead of what might happen in this way. She helped me understand in a deeper way one of the key things that cause us to sometimes lose our ability to think clearly and make good decisions in the face of an uncertain future.

That being said, my philosophy on the subject of uncertainty is, I believe, somewhat different than Marilee’s and in particular, I think we differ in our analysis of what allows us to overcome the fear and other obstacles that keep us from living comfortably in an uncertain world.

This is in no way a criticism of the value of what Marilee provides or the way she does it. For many people, Marilee’s approach to developing a “Learner Mind” is highly effective. The issue for me, however, is that in Marilee’s workshops (or at least the one I attended), there is a lot of homework, and I was asked to work harder than I was prepared to when I accepted her invitation. For many, I realize that that, by itself, is a good thing, but in this case my personal idiosyncrasies prevented me from getting the full benefit of Marilee’s training.

My problem is that fundamentally I don’t like homework – I got away with not doing much in school and in many cases didn’t see the point of why it was assigned in the first place. My father and I had arguments about that, and like many things, he was more right than wrong in lecturing me for not doing my homework, but still, somehow, I came out ok.

Many believe that our minds can be trained to be curious, and maybe they can, but I think our ability to ask good questions can also come from a different source – specifically the wealth of natural curiosity that abounds within us, and just needs to be unlocked and allowed to emerge naturally.

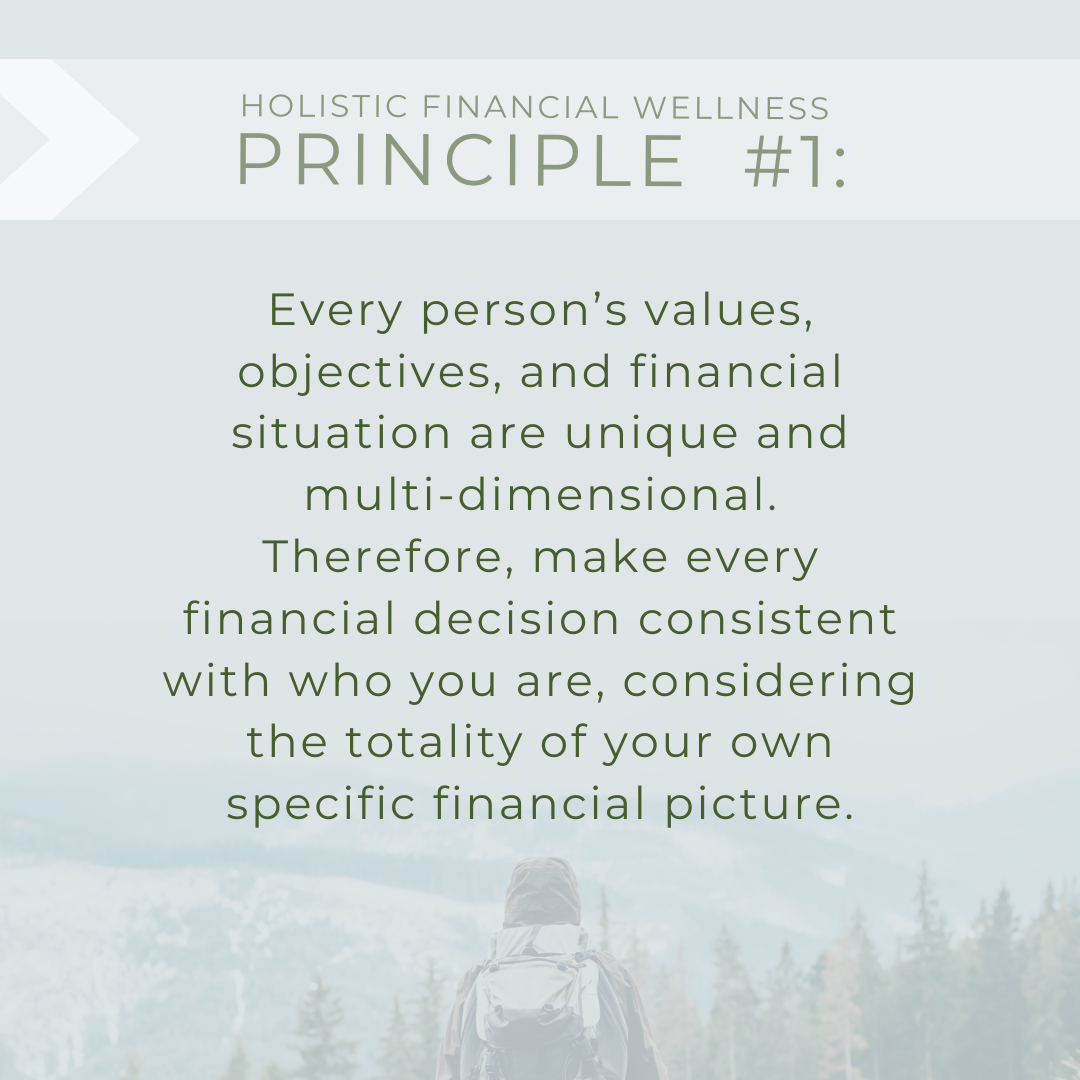

For me, curiosity and disciplined practice/training just don’t mix, though just like Holistic Financial Wellness Principle #1 states, we are all unique individuals and different approaches to getting better at making good financial choices are appropriate for different people. Many of us welcome the discipline and skill development that Marilee imparts – and she is an extraordinarily good trainer in that regard, but I take a somewhat different approach to my own path to getting comfortable with “not knowing”.

Specifically, I believe that humans are at their best when they get in touch with that wild, playful, undisciplined adventurous side – a side that, if we were lucky, we enjoyed as a child and can still return to. For me at least, that’s where my curiosity lives.

So how do you get more curious and want to ask the questions you need to ask – about your job, your 401(k), your bank, or even cryptocurrency? I don’t believe there is a single answer to that question, but my approach is different than Marilee’s. Rather try to train myself to be curious, I simply listen to my own inner voice and pay attention to what I hear. Am I falling prey to anticipation when I think I know what is going to happen? Is it fear which keeps me from thinking about what might happen? Or is it a combination of both – throwing me off track as I hear myself say “I am afraid and don’t want to think about what I am sure will happen (in the market, the economy, my company, and even my family).”

It is also important to realize that being curious won’t necessarily help you to figure out what will happen next. Fundamentally, to make good financial decisions in an uncertain world, we need to remember that while the future is unpredictable it is not unimaginable. Being curious and open-minded is just the first necessary step towards financial wellness.

In the end, I believe that Marilee and I agree completely that to make better financial choices you need to be curious enough to ask the right questions and open-minded enough to listen to the answers.

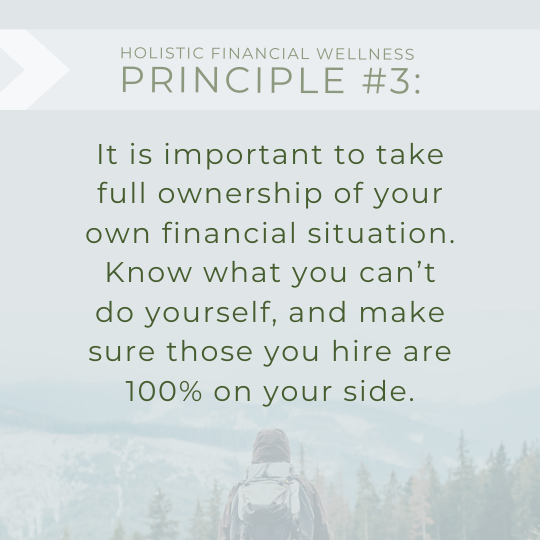

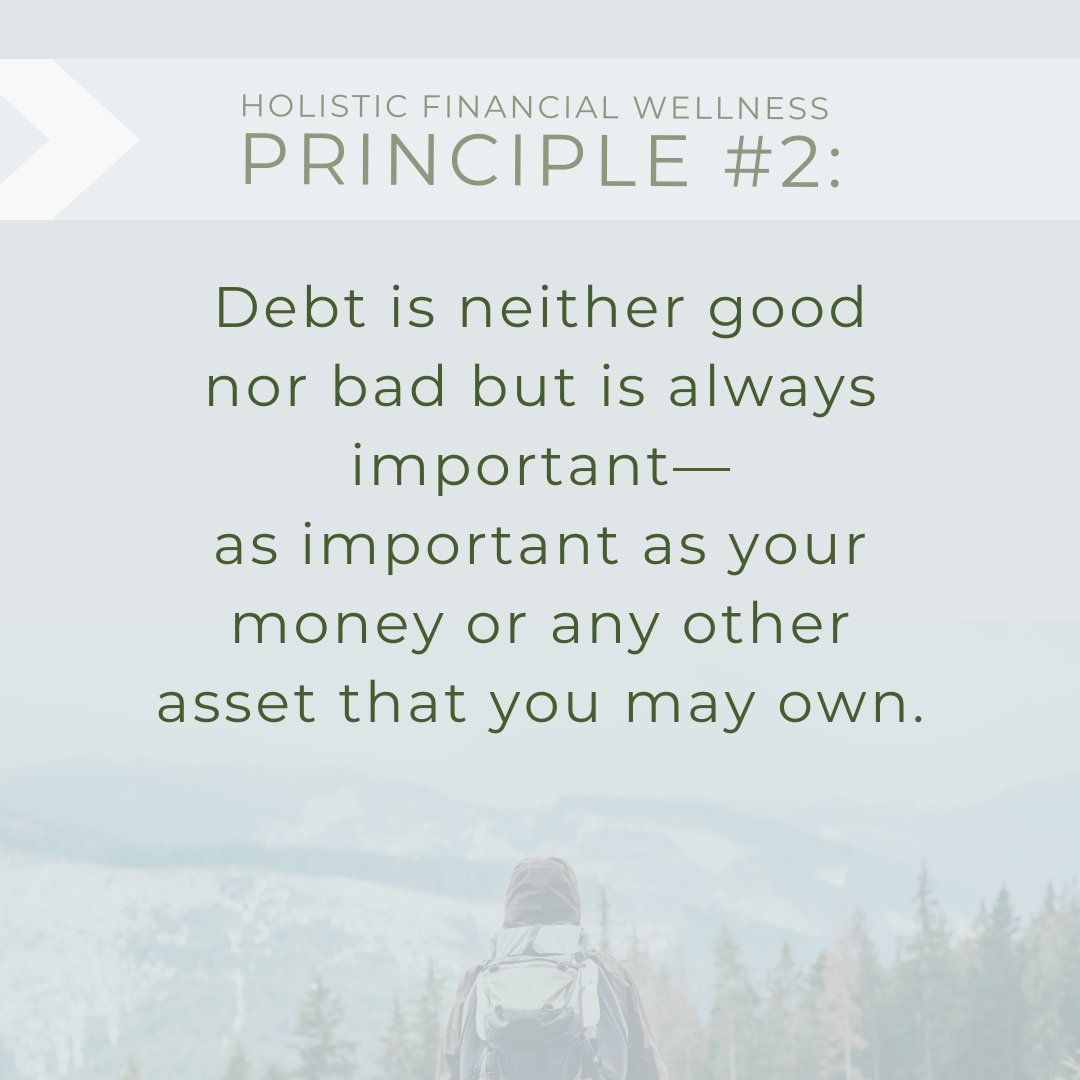

That is what the Holistic Financial Wellness Principle #4 is all about.