My minder, social media coach, cheerleader, and overall brave new world guru, Julia Page must take some responsibility for this essay about Holistic Financial Wellness Principle #5.

It’s not that she told me what to write. One of the reasons I hired her is because she is so good at letting me be me. I love to write but breaking my thoughts into bite size memes doesn’t come easily to me, and while Julia tolerates my long windedness, she told me that I needed to discard my original draft and write a crisper, more focused version of this essay so that it would be both easy to read and helpful to readers who struggle with money issues.

I understand that these days, people have very little time to devote to reading – maybe checking out a link during a break, listening to an idea passed on by a friend, or maybe, if you’re lucky, finding an insight from the avalanche of information in your daily feed that will help you solve a problem that is keeping you from making progress.

This seems to be the state of the world and a consequence of an acceleration and a compression of the time we are given to solve the problems we face. That is neither good nor bad, and I don’t spend much of my time trying to figure out who or what is to blame – it is just a feature of the world we live in.

And so, in this essay, while just as long as the others in this series is focused on the essential task of trying to help you understand the essence of HFW#5 and why it can help you survive and thrive financially.

Holistic Financial Wellness Principle #5 is perhaps the most difficult and counterintuitive of the principles I espouse. In addition to using the word “antifragile” – a word that doesn’t appear in any dictionary you are likely to have in your house, it relies to a great degree on the work of Nassim Taleb, a man who is not easy to understand – particularly the mathematics that forms the rock-solid basis for his conclusions. But just because Dr.Taleb is hard to understand doesn’t mean it is hard to understand what will help you survive and even thrive in a world of Black Swans and fat-tailed distributions. You won’t learn it all here, but at least you’ll get a taste of what Chapter 8 will tell you if/when you end up reading Money Mountaineering.

.

.

Fragility, Hidden Risks, and How the World Changes

“I know that history is going to be dominated by an improbable event, I just don’t know what that event will be.” ― Nassim Nicholas Taleb, The Black Swan: The Impact of the Highly Improbable

What Dr. Taleb says above has been shown to be the case again and again in the last several thousand years, but it took reading his three books (Fooled by Randomness, The Black Swan, and Antifragile) for me to really get it and start incorporating his insights into how I structured my financial life.

Fooled by Randomness taught me that most of the Probability and Statistics I learned in college and as an actuary, was, at best, incomplete, and, often, downright misleading. The Black Swan was sobering, but not as disorienting to me since as an actuary I was used to helping my clients protect themselves against things that almost never happen, but reading it helped me appreciate that the low probability/high impact events that do happen are the things that, in fact, change the course of history. This was hammered home by both the Financial Crisis of 2008 and the Pandemic of 2020 – which I think most of us would agree were exactly the kind of Black Swan events that Dr. Taleb talks about.

In 2012 Nassim Taleb published his third book Antifragile. By then I was enough of a fan to buy it as soon as it came out and devoured it immediately, learning that “fat tailed distributions” weren’t just the place where Black Swans come from, but are also the breeding ground for events that can make you stronger when the world changes in dramatic and unexpected ways.

Understanding Nassim Taleb and Using his Insights

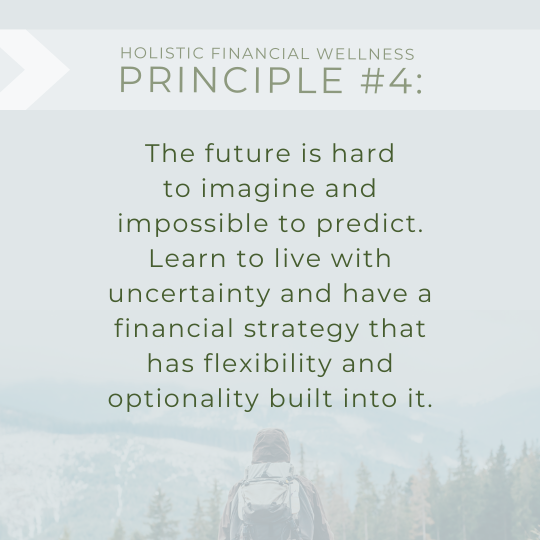

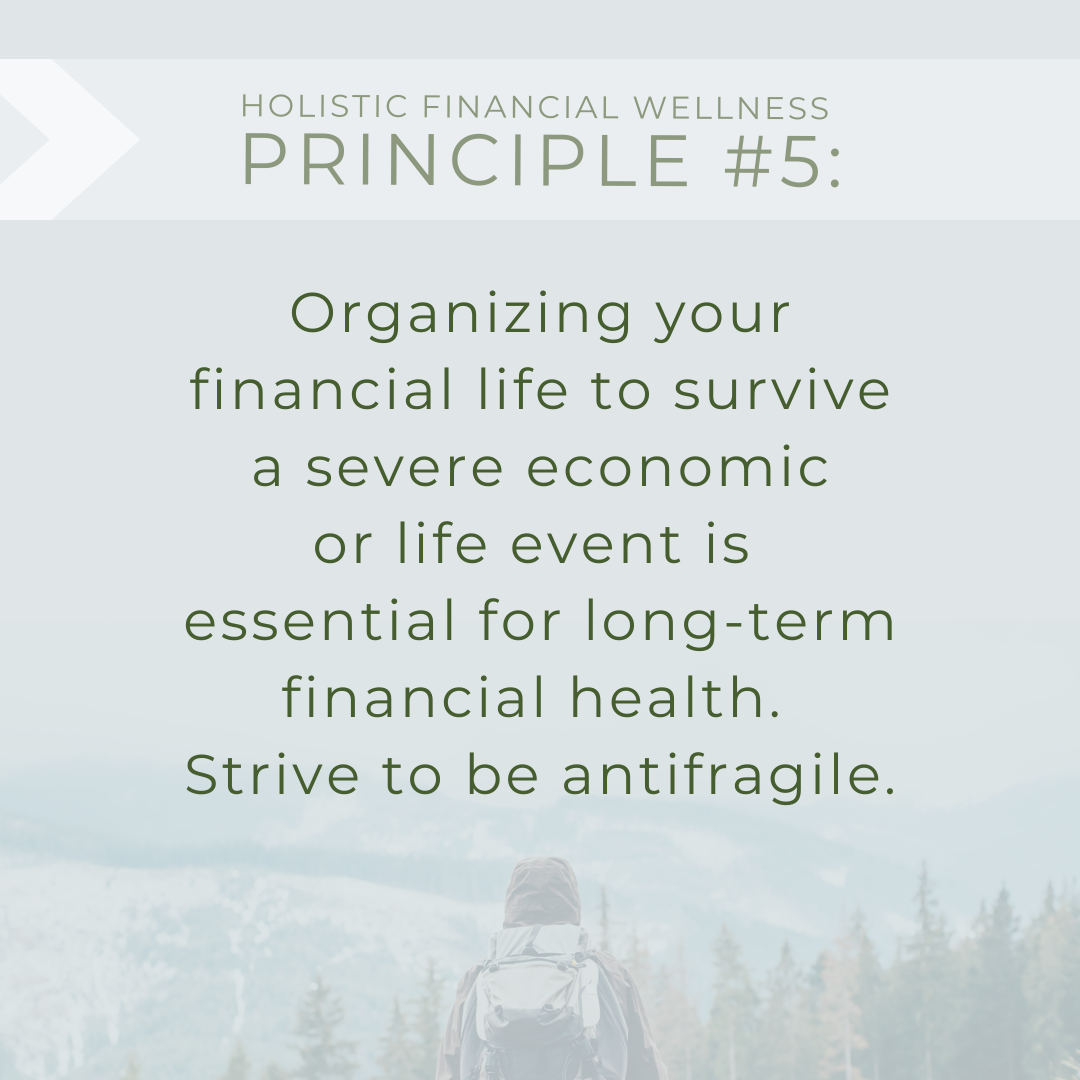

Holistic Financial Wellness Principle # 5 says:

“Organizing your financial life to survive a severe economic or life event is essential for long-term financial health. Strive to be antifragile.”

What that means is first and foremost, that you should prepare to survive a potential Black Swan event, and second that you should try and structure your assets and liabilities in such a way that you benefit rather than suffer from the volatility that long term exposure to markets governed by fat tailed distributions will inevitably produce.

When the Financial Crisis of 2008 occurred, I was living and working in Paris, France and had the benefit of being able to watch the financial world crack and crumble from a safe distance. For the first time in my life, I realized that almost everyone who was responsible for “managing” our economy and keeping the global financial system operating didn’t know what was happening and, worse, didn’t know how to stop the wildfire that was destroying corporations, banks and even a giant insurance company (AIG) along with the financial lives of millions of people who were losing their homes, their jobs and even their pensions and retirement savings.

It is easy to forget how scary and uncertain those times were, and though our economy and the markets have recovered, the experience told me that not only can it happen again, but eventually it will happen again – not a “real estate bubble induced financial meltdown” but something else just as unexpected and just as world changing. When the Pandemic of 2020 came ashore and crashed our economy so severely that the country’s unemployment rate increased from under 4% to 14.7% in one month (something that had never happened before) I was ready, or, if not ready, at least prepared enough to not have to worry about by income or my ultimate financial survival.

Now that the economic crisis associated with COVID has passed, or at least morphed into something else, we are beginning to forget again how scared we all were about our money and our jobs and feel that things are getting back to normal – economically at least. Maybe so, but I still think the lessons of these two Black swan events should be incorporated into how we manage our financial lives and I believe that keeping Holistic Financial Wellness Principle #5 in mind can help.

So, what did I do to prepare, and why am I feeling ok financially?

It is because I took a “barbell” approach to my financial life to become antifragile and, through redundancy and insurance, made sure that if one part of my personal balance sheet disappeared, I would still have enough resources to sustain myself and rebuild anything that was lost.

I will tell you, in a minute, a little bit about what I did, but first I want to go slightly deeper into the insights that informed that strategy. From Dr. Taleb’s books I learned that

- Pronouncements by investment experts about the future behavior of many investment markets that are based on “historical patterns” including those based on capital market assumptions that come from “sample means, sample variances, and sample correlation coefficients” are almost certainly wrong because one of the statistical consequences of being in a fat tailed distribution is that you will never be able to collect enough historical data to know just how likely or unlikely extreme returns (positive and negative) will be in a given market whether it be soy bean futures or cryptocurrency.

- The situation is not as hopeless as the above would suggest because it is possible to gain some insight into the nature and extent of the “fatness” of the tail of a given distribution, and, in particular, it is often possible to determine whether the likely nature of the distribution provides an opportunity for profiting from volatility

It is not at all obvious how to take advantage of item 2 from a theoretical perspective, but as a practical matter I believe that the concept of using a “barbell strategy” as I describe in Chapter 8 of Money Mountaineering is something to consider.

Beginning in early 2008 I started to model my financial strategy along these lines, first spreading my money among different banks eventually having significant percentages in 4 different major institutions. At the same time, I started to radically diversify my sources of retirement income, eventually obtaining Life Insurance and Annuities from 3 different major insurance companies as well as a Charitable Gift Annuity and a Charitable Remainder Trust from my old school which has an endowment of almost $500 million backstopping the life income that they will begin paying me when I turn 65. It goes without saying, that I also made sure that I had enough insurance to protect me against known contingencies like death, disability and other hazards that are more easily imagined (fire, theft, and being sued).

For the next few years, I didn’t worry too much about my long-term financial security. I had a secure and stable spot in the actuarial profession and was confident I would have enough income to meet my needs and then some until I had to stop working as a W-2 employee. That didn’t happen until 5 years ago, when in 2016, my company merged with another giant consulting/brokerage firm, and I decided to take early retirement.

As soon as I retired, I organized my financial life as two barbells. On the one hand I have a collection of diversified assets that will provide me with bullet-proof secure and steady income that will be enough for me to live on if I lose everything else. They include the annuities I described above, as well as cash value life insurance, the Pension benefits that I now receive from the companies I had worked for as an actuary and a an old 401(k) plan that is 100% invested in US TIPS (“Treasury Inflation Protected Securities”).

The above investments comprised a large percentage of my assets, so I don’t have a lot of extra cash to deploy to the other barbell, but what I did have, I deployed into highly speculative investments (mostly collectibles) whose payoff will likely follow “Pareto’s rule” –a form of fat tailed distribution where most of what you invest in earns nothing or less but every once in a while, you hit a “home run”. Since I didn’t have enough investable assets to construct a true second barbell (e.g., by becoming an “angel investor’ in multiple start-ups) I instead decided to invest my time in lots of different side ventures, most of which sill likely come to naught, but any one of which could substantially reward me if they are successful. That is how I apply Holistic Financial Wellness Principle #5.

Get Ready for the Future

These days, Nassim Taleb continues to make his writing available to all who are curious to read about his ideas in real time. Specifically, if you go to academia.edu and follow him, you will be able to read many of his recent papers, both technical and not. Like many things in life, working through what Nassim Taleb has to offer the world is not easy, but for many of you it could represent a very smart investment of time and energy.

To provide one recent and particularly timely example, in June of this year, Dr. Taleb posted this paper about bitcoin:

https://www.academia.edu/49313911/Bitcoin_Currencies_and_Fragility

This one is not that difficult to read, but if you are not very “mathy” then the explanation of the paper posted by Michael Edesess on Advisor Perspectives in July explaining Dr. Taleb’s work should help. You can read it here:

https://www.advisorperspectives.com/articles/2021/07/18/why-nassim-taleb-says-bitcoin-is-worthless

In the last few years, many of my friends and colleagues have wondered why I speak about Nassim Taleb so frequently and with what is sometimes perceived as “missionary zeal”. I hope this essay has provided at least a partial answer.

The truth is that, if and when a true Apocalypse comes, none of what I or Dr. Taleb says will matter much, but until that day arrives, Dr. Taleb’s insights are well worth absorbing– particularly his understanding of the Fat Tailed Distributions in which we find ourselves embedded in. For me, the message is clear, and to paraphrase what I posted a while ago about risk management in a world governed by fat-tailed distributions:

“If you live your life believing that Life follows a Normal distribution, you will find that things almost never turn out as badly as you fear, except when they turn out much, much worse.”

But things can also turn out much, much better than you expect and that is where antifragility comes in.

Perhaps the best way I can explain my approach is to quote the advice my father used to give me throughout my childhood– “Hope for the best but prepare for the worst”. That and his advice to me shortly after I graduated college to “keep as many irons in the fire as you can” are two of the teachings that have allowed me to survive and thrive, in the world of money for over 40 years.

That, essentially is what Holistic Financial Wellness Principle #5 is all about.